The firm’s boundaries define what the firm does. Boundaries can extend in different directions: horizontal and vertical. The firm’s horizontal boundaries refer to how much of the product market the firm serves, or essentially how big it is. The firm’s vertical boundaries refer to the set of activities that the firm perform itself and those that it purchases from independent firms in the market.

An understanding about concept of firm’s boundaries is clearly critical for formulating and assessing strategy. Strategy is fundamental to a successful organization. Much can be discussed about strategy from multiple lenses, such as mathematical game theory, psychology, organizational behavior, political science, or even anthropology. One of the many lenses is economics. Economics is distinctive in considering relationship among decision makers, goals, choices, and outcomes in the situation of business rivalry. The nature of economics as the science of constrained choice can be useful to build logical insight, linking conclusion derived from economic reasoning with the assumptions used in an analysis.

Below are the slides about horizontal and vertical boundaries of the firm. These slides were prepared for Economics of Strategy class in Prasetiya Mulya Business School week 3 and 4. Economics of Strategy is a subject that aims to establish foundation of strategy through discussions on concepts, mainly, related to economics.

As 2015 approaches, I think it would be interesting to discuss about the ASEAN Economic Community (AEC) which is set to be introduced next year. The ASEAN Economic Community is a regional economic integration in Southeast Asia that has objectives to create a single market and production base facilitating the free flow of goods, services, labor and capital.

In 2007, ASEAN’s leaders had declared strong commitments towards accelerating the establishment of AEC and since then the ASEAN countries gradually lower their import duties among them and targeted to become zero for most of the import duties in 2015. If we talk about achievement to date, more than 70% of intra-ASEAN trades are now trade-free and less than 5% subject to tariffs above 10%.

However there are still remaining challenges such as removing barriers to trade in sensitive areas like agriculture and steel, removing border barriers as well as removing behind-the-border constraints related to logistics, transport, infrastructure problems, weak institutions and adopting harmonized standards on competition policy and intellectual property rights.

In addition that, the other challenge is regarding the development divide between less-developed economies such as Cambodia, Lao PDR, Myanmar and the other economies in the region. The development divide should be narrowed so those countries remain engaged, no countries to lag behind and all countries in ASEAN are on a par with each other. It is important because by having this integration; there will be both winners and losers, at least in the short run.

If we look through those challenges mentioned before, many believe that the 2015 deadline will not be achieved. I think we should not view the year of 2015 as a hard deadline but rather a milestone within a longer journey. We could use the year to serve more as a benchmark of progress because depending on the speed of progress, more measures for integration can be undertaken at 2015 and beyond.

“It cannot be completely done by a certain date, but the reason why they set the date is also to get everybody across the region committed to a certain timeline. Even when it comes to the date and the task cannot be fully accomplished but it is ongoing.” Ong Keng Yong, former Secretary General of ASEAN

Although the AEC is a government-led agenda, the AEC cannot succeed without fully engaging the business community and the public at large. Thus, we need to look at the impact of AEC towards business sector. In fact, the private sector is kind of skeptical about the AEC realization and the firms in the region are not convinced that it will actually help to boost their business.

Based on the ISEAS-ADB survey that conducted in March 2012 with total of 381 firms in nine ASEAN countries, 55% of the respondents said they were not aware of AEC 2015 and 77% said they never fully engaged and benefited from the low tariff privileges. Some factors that prevent the business sector to take advantage of this integration are mostly because of lack of information on how to make use of the new tariffs that have been put in place and administrative costs in the form of excessive bureaucracy, different regulatory standards, etc.

ASEAN needs to encourage private sector to be more engaged and contribute to increase the effectiveness of the implementation of the AEC. Some policy suggestions that can be considered are the following: (1) Establish National AEC unit one stop shop for timely AEC related information (2) Explain the advantages of AEC to private sector and also get rid of the fear of perception from some businesses who has lack of culture of competition (3) Cross-country simplification, harmonization and standardizing of business rules and regulation.

ASEAN has in fact made some progress towards achieving an economic community, but there are several challenges to meet that deadline of 2015. Let me conclude this article with some optimism. We could see the AEC 2015 as means rather than ends because the process of regional economic integration requires individual country’s structural reform. At the end of the day, even it does not happen, we as countries still benefit from the effort to be better and more competitive. The process towards the integration may not be completely and perfectly accomplished but at least we are moving to the right direction.

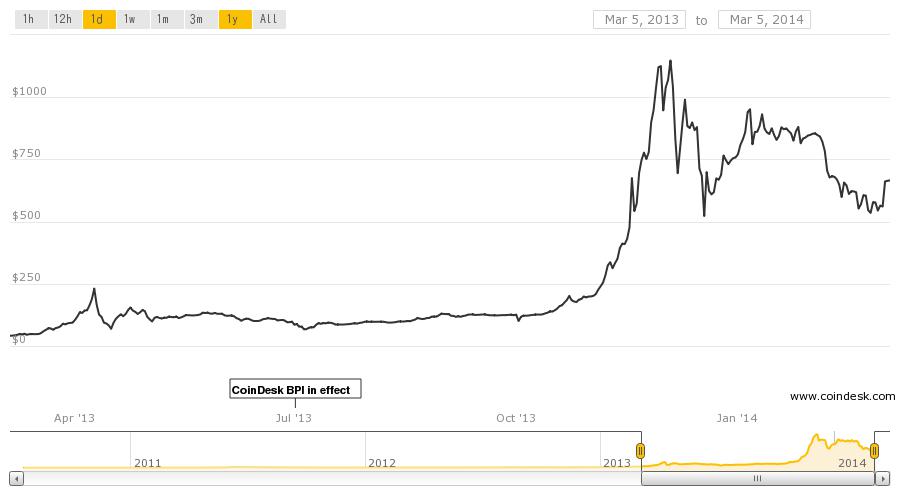

Bitcoin has gained so many controversies all over the world. In the last few months, the popularity of Bitcoin has skyrocketed due to its hundreds of times increase in price. Bitcoin made headlines on November 29, 2013 as the price of a single coin hit an all-time high, recorded at $1,242 per coin compare to the first time it introduced in 2009 which nearly had no value.

Since Bitcoin has attracted a lot of attention, a lot of people are arguing over it now. There are debates between economic schools, between politicians, between programmers. Some people are smart, some are misinformed. Some say it’s a digital gold, some say a currency, other say they’re just like tulips. Some people say it will change the world, some say it’s just a fad. Well, I have my own opinion about it.

Just to make sure we are in the same page, here’s the explanation about what Bitcoin is and how it works. Bitcoin is the first digital currency that can be used in peer-to-peer exchange system, but certainly not the last. I could say that it is a fascinating idea with extremely controversial subtexts. The transaction is not backed by any central bank; it is traded on a number of exchanges privately and generated by a process called mining. Theoretically, it is possible for all computers across the world to run the software and locate Bitcoin by solving an algorithm. The Bitcoin owner has a virtual wallet and a transaction can be made through the use of key identification, but not the identity of the user.

It seems that Bitcoin can solve many problems from which our current currencies suffer while also create problems that consumers, bankers and economists have never had to deal with before.

Bitcoin Upsides

Low Inflation Risk

Unlike in traditional paper economies where governments can print as much currency as they need, the Bitcoin system is designed to be finite. Growth of the Bitcoin money supply is determined by the Bitcoin protocol, in this way inflation is kept in check. Currently there are 12 million Bitcoins in circulation and the rate of new Bitcoins will be halved every four years until the maximum total supply of 21 million Bitcoins which expected to be happened in 2140.

Efficiency

Since there are no middlemen involved in transaction and it is not tied to any country or subject to regulation, the transaction fee of Bitcoin is really low. The cost is so much cheaper compare to credit cards (3% of transaction value), PayPal and other online payment systems. In addition, remember that Bitcoin is digital. With a virtual wallet, money is easy to store and carry. People can send 1000 Bitcoins or 10 million Bitcoins or even 0.000001 Bitcoins easily by a click of a button, doesn’t matter whether one person is in Jakarta and the other is all the way in New York.

No Government Dependence

As Bitcoin is a global virtual currency, it doesn’t depend on government collapsing or re-emerging. Although in the theory money is not a political product, in the reality most of all currencies created by human beings will become political at some point.

Niche Market in Global Financial System

Bitcoin fits an important niche in global financial system, there are still a lot of people who can’t access the global financial system but they can access Bitcoins. It is an attractive investment because it is a store of wealth, in a completely free market. Some people buy Bitcoins hoping that their value will go up. There is still room for improvement but the Bitcoin is still in its infancy.

Untraceable

The final upside is the first downside. Bitcoins can be used to buy merchandise anonymously. No one knows who you are and the Bitcoins can be sent to purchase or sell with genuine anonymity. Furthermore, unless the owner of Bitcoin tells someone about their Bitcoin wealth and their passwords, there is no way for others to know how much Bitcoin wealth you have.

Bitcoin Downsides

Untraceable

With the characteristic of untraceability, Bitcoin can be used for money laundering and for transacting illegal goods such as drugs, guns and other items.

Lost Bitcoins are Lost

If people lose their Bitcoins, they will have lost them for good. There is no system yet to recover the lost or stolen ones.

Price Volatility

Bitcoin markets are not for the faint of heart as the prices are extremely volatile. As of this writing, Bitcoin price is about $660, it was ranging anywhere between $500 and $1200 per Bitcoin in the last two months. Each day brings a different price or so it seems since price can easily fluctuate 2% to 5% within minutes for no apparent reasons. This leads to a major challenge: Bitcoin’s value is not stable. It has fluctuated wildly, which makes it not suitable as a long-term currency. These fluctuations are often due to speculation which happens because the supply is fixed (only 21 million will be mined) and the demand is erratic.

Speculative Bubble

Bitcoin can be traded as an investment by speculators who expect growth in popularity and value. The high risk of engaging in speculation has gone beyond a potential loss of Bitcoin value since it becomes vulnerable to theft and hacking as well. Two lead Bitcoin software developers, Gavin Andersen and Mike Hearn had warned that bubbles may occur. One financial journalist has correctly predicted one of the bubbles which burst in April 2013.

Threat from Government Intervention

In addition to these downsides, Bitcoin is also expected to have serious problems with governments. Under the best circumstances, Bitcoin is expected to be immune from government intervention, especially regarding to its legality. However, when the governments begin issuing rules against Bitcoin, its market value will be plummeted.

Based on the upsides and the downsides, I could say that Bitcoin is not ready to be a currency. Even though others who mistrust their national currencies and central banks have seen Bitcoin as a safe haven from inflation, capital controls and international sanctions, the volatility of its value limits Bitcoin to act as a currency. However, this doesn’t prevent Bitcoin to be used as a medium of exchange. There is no cheaper way to pay for goods internationally than Bitcoin. As consumers continue to engage in digital marketplaces, Bitcoin becomes an advantageous option. There are also thousands of Brick-and-Mortar businesses, up by 300% since November 2013 which are now accepting Bitcoin. With low fees and its efficiency, Bitcoin has potential to address some of the biggest issues in our financial system today, especially when it comes to micropayments.

It will be very interesting to see what the future of Bitcoin is. Stay tuned!

The Central Statistics Agency recorded that Indonesia’s economy grew by 5.78% in 2013. Even though it was the slowest pace for the last four years, improvement has occurred in all economic sectors. The highest growth recorded in the transportation and communication sector, which stood at 10.19%, followed by finance, real estate and services sector which grew by 7.56%. Meanwhile the country’s GDP growth without oil and gas reached 6.25%, higher than the overall GDP growth.

The economic slowdown was not so bad; some argued that GDP growth of 5.78% can be categorized as high compare to 5.6%, the 2013 economic growth projection. However, we have to remember that economic growth should be seen by not only quantitatively but also qualitatively.

Unfortunately, GDP growth in 2013 was not a high quality growth because it was not supported by tradable sector (goods). Tradable sector consists of agriculture sector, mining and quarrying sector, and manufacturing sector. This leads to minimum worker’s employment absorption in the economy.

The high quality growth should create employment and reduce poverty. Otherwise, even high growth could lead to wider inequality. In 2013, most of Indonesia’s economy growth was supported by non-tradable sector (services) since the growth in that sector was above the GDP growth itself meanwhile the average of tradable sector growth was below the GDP growth.

Growth does not guarantee poverty reduction. The number of people living in poverty depends on the level of GDP per capita and the degree of inequality in society. Even countries with high level of GDP per capita will have poverty if they are characterized by extreme inequality.

Reducing poverty therefore requires either boosting GDP per capita or reducing inequality by redistributing resources towards the poor. In recent years, the emphasis in poverty reduction has switched away from redistribution and towards GDP growth. One thing to keep in mind is GDP growth can theoretically have various effects on poverty.

Whether economic growth will automatically reduce poverty depends on its relationship with inequality. If the benefits of GDP growth accrue only to the rich, then growth will increase inequality and leave poverty unaffected. It may even be possible that growth in modern sector of the economy leads to declines in traditional sectors where the poor are mainly based. In this case GDP growth produces widening inequality and higher level of poverty – low quality growth.

Alternatively, if GDP growth does not affect inequality, then everyone enjoys the same proportional increase and poverty falls. But the most efficient way to reduce poverty is through pro-poor growth. This kind of growth is GDP growth that reduces inequality so that more of the benefits accrue to the poor leading to a faster in poverty.

To conclude, we should not judge Indonesia’s economy growth solely from the number whether it is high or low but also from the quality itself. Boosting GDP growth is important but how the growth affects inequality and poverty also matters to make Indonesia’s economy better.

In the last few decades, countries tended to liberalize their financial system. Loosening credit controls and interest rate controls, reducing entry barriers and reserve requirements, privatizing the banking sector, promoting foreign investment, in general countries have moved to the financial liberalization era.

Financial liberalization refers to the deregulation of domestic financial markets and the liberalization of the capital account. Commonly, financial liberalization is viewed to promote economic growth because it strengthens financial development. However, in contrast, some studies find that financial liberalization induces excessive risk-taking behavior, increases macroeconomic volatility and leads to more frequent crises.

Based on a study of 53 countries from Demirguc-Kunt and Detragiache in 1998, 78% of financial crises occurred in the period of liberalization. The study shows that when a country liberalizes its interest rate, it is more likely that country experiences a banking crisis.

This fact motivates me to closely analyze the relationship between financial liberalization and financial crises. I also want to contribute to the literature in this area by not only focusing on banking crisis but also adding some other types of crises such as debt crisis, inflation crisis, currency crisis and stock market crash. Since the countries that experienced these crises consist of both developing and developed countries, I want to find out whether the effect is the same for developing and developed countries.

The dataset which consist of 35 countries data from 1973-2005 is estimated by the linear probability model combined with fixed effect and IV probit model. I use the dummy variable for various crises as dependent variable and the financial liberalization index as the main explanatory variable. The financial liberalization uses seven different dimensions of financial sector policy that affect the financial liberalization process. The following seven dimensions are credit controls and excessively reserve requirements, interest rate controls, entry barriers, state ownership in the banking sector, capital account restrictions, prudential regulations and supervision of the banking sector, and securities market policy.

After done with the regression, I can say that financial liberalization affects various financial crises differently.

Banking Crisis

For banking crisis, the effects of financial liberalization in both developing and developed countries are statistically significant for all period lags. The signs of the coefficients are positive, meaning that when a country is more financially liberal the probability of getting into a banking crisis increases. This result confirms the previous study from Demirguc-Kunt and Detragiache that banking crises are more likely to occur in a liberalized financial system.

In general, one year lag has the highest effect among the others and continues to decrease until five years lag. It means that financial liberalization has the greatest effect on crises when the lags between them are short and smaller effects in the longer period partly because financial liberalization stimulates institutional reforms.

In particular, we can compare marginal effect of financial liberalization on banking crisis between developing and developed countries. In all five years period of lag, the developing countries have a higher risk getting into banking crisis rather than developed countries. It can be explained when a country liberalizes its financial system by reducing regulations in the banking and financial sector and allows international capital to move more freely, it can lead to excessive risky profit taking actions by bank management and investors which makes the bank sector more fragile.

Debt Crisis

Similar with the result from banking crisis, the effects of financial liberalization on the probability of a debt crisis are highly significant for all countries in all five years period of lags. Financial liberalization increases the probability of the occurrence of debt crises in both developing and developing countries but the effect is bigger in developing countries.

A possible explanation regarding this result is when a country is more financially liberalized, people in that country can not only borrow from domestic sector but also from abroad. It leads to overborrowing and overlending that may increase the possibility of illiquidity and insolvency of the debts. Previous studies also have similar results, financial liberalization increases the probability of a debt crisis because financial liberalization allows more liquidity to enter an economy and it increases speculative financing significantly thus increasing the chance for default. When the outflow of international capital becomes more likely, the crises grows faster.

Inflation Crisis

Different with two previous crises, the effects of financial liberalization inflation crisis in developing countries have a negative sign which means that liberalization can decrease the probability of hyperinflation in developing countries. It may be explained because when developing countries open their countries to the international financial market, they do not have to depend on printing money (which can cause inflation) when they want to raise their revenue since they can borrow from the international capital market. However, the effect is different for developed countries. Financial liberalization increases the probability of inflation crisis in those countries. In general, the effects are statistically significant except for the four years lag in developing countries and five years lag in developed countries.

Currency Crisis

In currency crisis, the effect of financial liberalization is significant only on developing countries and the result shows that it decreases the probability of currency crisis. It means that when people increase the liberalization of their financial system, the likelihood of a country experiencing a big depreciation decreases. Somehow it contrasts with the explanation that developing countries usually peg their currency and because of bank rushes that may happen because of political events, they cannot defend their peg, float their currency and experience a huge depreciation.

Stock Market Crash

In the case of stock market crash, the effect of financial liberalization is not significant in developing countries in all period of lags. On the other hand, the regression from developed countries show contrast result. Financial liberalization significantly increases the probability of developed countries in all period lags. A possible reason why financial liberalization has a really contrasting effect between developing and developed countries is simply because stock markets in developed countries are well developed compared to developing countries that may not have an established stock market.

When developed countries liberalize their financial system, regulation over banking and financial institutions including the stock market is reduced. It encourages the investors to utilize profit taking actions even more. In addition to that, when there are free capital flows into and out of the countries without proper regulations, there will be hot money and short term investment from abroad. The risk for the country will be high because foreign investors can pull out their money easily and leave the countries with a crash in their stock market.

In OPEC case, when cartel firms gain profit, they reinvest profit in new capacity by exploring new oil mining or investing in the new machine which able to produce higher level of output. When the demand for oil is relatively constant, reinvestment in new capacity leads to a higher excess capacity. The capacity to produce oil is underutilized and each country that joins Organization of Petroleum Exporting Countries (OPEC) has a higher excess capacity.

Underutilization makes an incentive for cartel members to use the excess capacity. In order to prevent that, the cartel makes side payments for the members. A side payment is made by one or more parties in a cartel agreement to other parties to induce them to join the cartel. If a country in OPEC produces oil by using its fully utilized capacity, it will increase supply of oil in the market and if the demand unchanged, the oil price will go down. If the price goes down, the profit of oil producers will decrease and it will make all members become worse off.

In order to maintain the price level of oil, the oil producers should maintain its level of output as well. Basically, each country wants to get higher profit by selling high level of output from its own plant but the country can be induced to agree to a plan which includes side payments from the member based on production share. Side payments can compensate the profit opportunity that cannot be captured because of the restriction of output.

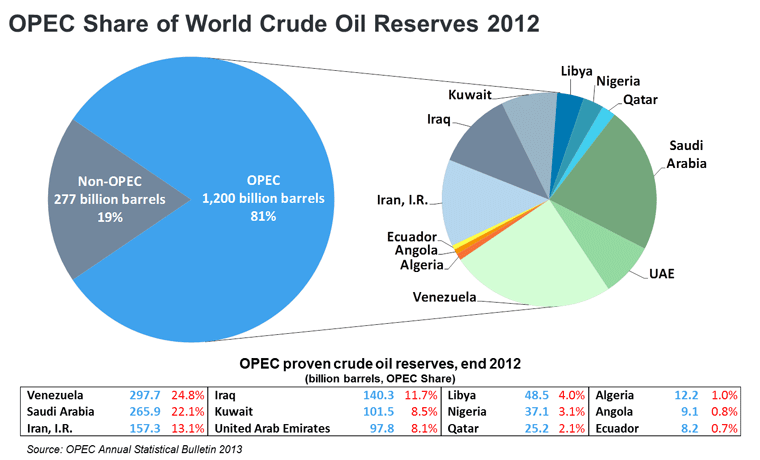

As the excess capacity increases, the side payments that are needed to compensate OPEC members also increase. The country that has larger OPEC share have to pay a larger portion of side payments as well. The diagram below represents OPEC share countries.

From the diagram above, the fact that Venezuela and Saudi Arabia have a big capacity to produce oil implies that it is costly more to these counties because they have to pay larger side payments to compensate other countries.

In addition to that, the higher excess capacity of OPEC countries is tempting OPEC member countries to cheat from the cartel agreement and increase the oil production. By doing this, the countries can experience economies of scale which leads to a decrease in average cost. With lower cost, the countries can get higher profit. If countries who cheat on the agreement has a relatively large capacity than the other, for instance Saudi Arabia, it can produce with the full capacity production, sell a lower price and do predatory pricing to other members.

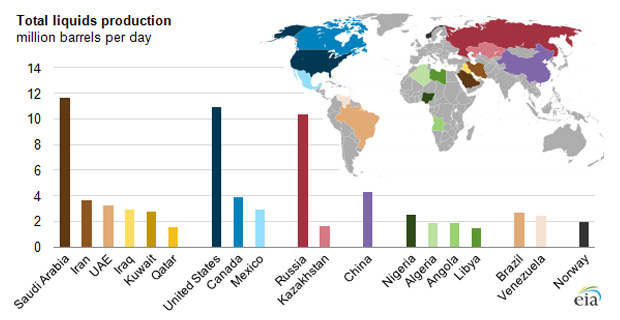

High burden of side payments and temptation to cheat on cartel agreement makes the cartel become more vulnerable and more likely to break apart. The other explanation regarding the destruction of cartel is the increase of competition from non-OPEC countries such as United States and Russia.

Source: Smart Planet Bulletin 2012

Increase in competition can drag the oil price down because of increase in supply. One of the factors of a high level of oil production from non OPEC countries is the increase level of oil exploration in those areas. The decrease in oil price internationally will reduce OPEC price as well in order to be able to compete with non OPEC countries. At the end, there is no further incentive to keep the cartel agreement.

There will be some impacts toward the long run viability of the cartel. In the long run, the cartel is unstable and difficult to sustain because there is a higher probability to breakdown. Whether members of the cartel choose to cheat on the agreement depends on whether the short run returns to cheating outweigh the long term losses from the possible breakdown of the cartel. The relative size of these new factors depends on how difficult it is for countries to monitor whether the agreement is being followed by other country. If monitoring is difficult, then the cartel members are more likely to cheat and the cartel will more unstable.

Several factors that make the monitoring become more difficult and thus make cartel to break down are as follow: a greater number of members, differentiated products, difference in production cost structure, fluctuation of market demand and low frequency of sales with high value contract.